The Crew (well, me specifically) received an invitation to watch the Brewers Association’s midyear economic update online today (Thursday). There was nothing earth-shattering from chief economist Bart Watson, but it was still interesting to see where the national trends are going and how those pertain to craft breweries in New Mexico.

A summary of the BA presentation is available online here.

Sales through the first two financial quarters of the year are down 2 percent industry-wise, but have trended upward from the first quarter to the second, as they are typically wont to do as winter/spring transitions to summer.

It continues a relatively static trend started in 2022, where the growth in the number of breweries is roughly the same now as the rate of closures. Craft beer has stabilized somewhat coming out of the COVID pandemic lockdown stretch of 2020-21.

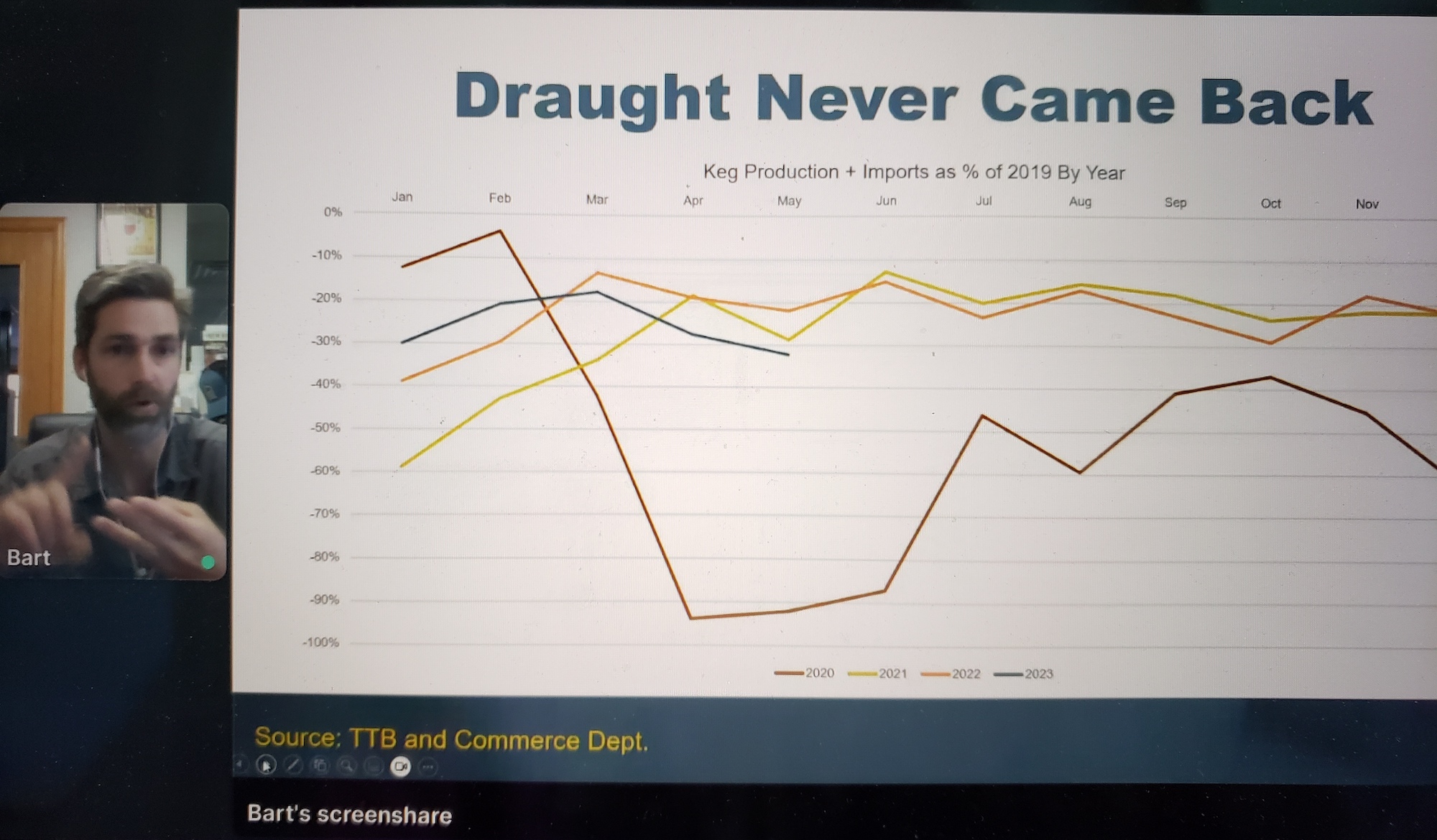

As Watson stated, it all starts fundamentally from demand. Consumer demand is down a bit, but it’s even more down among distributors and off-site accounts such as restaurants and bars. There has been a steady erosion in keg sales since peaking in 2014, but coming out of the pandemic, if things had remained on that same rate of decline, it would look different. How different? Breweries are producing 2 million fewer kegs than the previous rate of decline would project.

While those numbers are a bit alarming, other aspects of the economy of beer have stabilized. Taproom/onsite sales are steady. Breweries that produce less than 1,000 barrels per year are seeing steady growth, meaning that your favorite neighborhood pub may be doing better right now than a mid-size production-and-distribution brewery (there are exceptions, of course, and no, we have never been nor will the Crew ever likely be provided the raw financial data from New Mexico breweries; they are private companies and do not have to open their books to any media outlet).

Among consumers, the number of people drinking more craft and the number drinking less craft than before have basically evened out. The top reasons for people drinking less are largely driven by financial concerns, followed by living a healthier lifestyle.

For those wondering about the impact of hard seltzer sales, those are flat or even in decline, but other craft alcoholic beverages are seeing a significant increase. In particular, ready-to-drink canned cocktails are booming in the market right now.

Inflation in 2023 has caused craft beer prices, both draft and package, to rise, but food has still risen at a much higher rate across the board. Consumers are purchasing beer (and food) to go at a rate similar to 2019, so that has evened back out as more people are able to go out for a pint and/or a bite these days.

However, one thing the BA is watching in the upcoming fall/winter is the return of student loan payments, which greatly impact the primary craft-drinking demographics (ages 25 to 34 and 34 to 49). That could lead to a decrease in people going out and purchasing beer to take home.

Onsite visits to breweries, particularly the smaller ones, remain steady. So what is everyone drinking? You will be shocked, but IPA remains more than double that of any other style in craft beer.

Breaking it down further, the sub-categories of IPA seeing the most growth are double/triple/imperial West Coast IPAs and double/triple/imperial hazy IPAs. Pilsner is the only other category with a slight increase, but it’s very slight. However, Untappd check-ins (which are dominated by age 40 and up) are showing more lagers are being consumed than before, though IPA and stouts remain the top two categories overall on the app.

Among all the outside costs for breweries, most are seeing price increases level out, whether it’s in trucking/shipping costs, malted barley costs, or aluminum can costs. The one element still rising in price is CO2.

Toward the end of the session, those of us participating got to ask questions. Some were geared toward Tilray, the cannabis company buying the AB InBev “craft” brands (yes, Shock Top and Redhook and Widmer will now be considered actual craft again), and cannabis-infused beverages in general (it’s thriving the most in Minnesota, of all states).

My question related to a problem now facing breweries in New Mexico, and likely elsewhere. The skyrocketing cost of living in Albuquerque has left many breweries struggling to retain employees at the fairly low salaries that they can pay out (or are at least willing to pay out). With the average cost of a one-bedroom apartment now going above $1,000 a month in the metro area, many beertenders, packaging line techs, and cellarpersons are now looking for better-paying jobs simply to afford rent.

Watson responded with this: “One possible piece of good news is that housing costs are projected to come down. We’ve already started to see that (nationally). It’s one of the reasons total CPI (Consumer Price Index) is dropping. You raise an important point. This affects breweries in multiple ways. It affects them in terms of leases. Breweries built in areas with lower leases rates are seeing those areas become increasingly gentrified and owners now saying they’re forced to raise the rent. Leases are the most cited reason for closings. The landlord wants (five times) what they did before. For employees, this is going to continue to be a challenge. It’s going to be up to breweries to decide if they can pay more (in salaries). In general, we’ve seen wage costs go up, particularly in hospitality markets.”

So there is hope, but for the time being, it will remain an issue that breweries will have to find ways to deal with in Albuquerque, a city that is still sunny but no longer cheap.

Overall, it was neither a doom-and-gloom analysis, nor an overly positive one. Craft breweries face a myriad of challenges nationwide. The bar and restaurant industries have failed to rebound from the pandemic, so relying on off-site keg sales may be a thing of the past. Keeping distributors focused on craft beer instead of other craft beverages will remain an issue. Attracting new customers will be paramount, filling the gaps when people are priced out of the craft market, both as customers and as employees.

The bubble has not popped, but it’s still out there. We will see over the course of the remainder of 2023, and in the years ahead, just how our local breweries in New Mexico adapt and survive to the ever-changing economic climate.

Keep supporting local!

— Stoutmeister